Office of the Inspector General

Semiannual Report to Congress, October 1, 1999 - March 31, 2000

The Audit Division is responsible for independent reviews of Department of Justice organizations, programs, functions, computer technology and security systems, and financial statement audits.

The Audit Division (Audit) reviews Department organizations, programs, functions, computer technology and security systems, and financial statements. Audit also conducts or oversees external audits of expenditures made under Department contracts, grants, and other agreements. Audits are conducted in accordance with the Comptroller General's Government Auditing Standards and related professional auditing standards. Audit produces a wide variety of audit products designed to provide timely notification to Department management of issues needing attention. It also assists the Investigations Division in complex fraud cases.

Audit works with Department management to develop recommendations for corrective actions that will resolve identified weaknesses. By doing so, Audit remains responsive to its customers and promotes more efficient and effective Department operations. During the course of regularly scheduled work, Audit also lends fiscal and programmatic expertise to Department components.

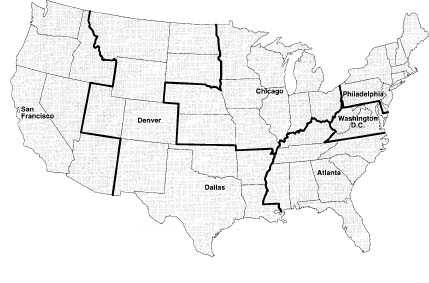

Audit has seven field offices across the country-in Atlanta, Chicago, Dallas, Denver, Philadelphia, San Francisco, and Washington, D.C. The Financial Statement Audit Office and Computer Security and Information Technology Audit Office also are located in Washington, D.C. Audit Headquarters consists of the immediate office of the Assistant Inspector General for Audit, the Office of Operations, the Office of Policy and Planning, and an Advanced Audit Techniques Group. Auditors and analysts have formal education in fields such as accounting, program management, public administration, computer science, information systems, and statistics.

The field offices' geographic coverage is indicated on the map below. The San Francisco office also covers Alaska, Hawaii, Guam, the Northern Mariana Islands, and American Samoa, and the Atlanta office also covers Puerto Rico and the U.S. Virgin Islands.

During this reporting period, Audit issued 159 audit reports containing more than $8.6 million in questioned costs and $4 million in funds to better use and made 293 recommendations for management improvement. Specifically, we issued 11 internal reports of programs funded at more than $165 million; 62 external reports of contracts, grants, and other agreements funded at more than $113 million; 13 audits of bankruptcy trustees; and 73 Single Audit Act audits.

COPS ARC Process Update

As discussed above, Audit conducts external audits of expenditures made under Department contracts, grants, and other agreements. The information contained in our external audits is intended to strengthen accountability in government by helping public officials, legislators, and citizens determine whether government funds are handled properly and in compliance with laws, regulations, and conditions stipulated in the funding agreement. During an external audit, we work with the auditee and Department management to develop recommendations for corrective actions. After the audit report is issued, Audit works with the auditee and Department management to correct identified weaknesses.

Our audits for COPS provide a significant example of this process. From October 1996 to September 1998, we conducted audits of 149 grantees receiving community policing funding under the Violent Crime Control and Law Enforcement Act of 1994 (Crime Act). In those audits, we noted numerous instances of noncompliance with grant conditions. COPS disputed many of our findings and appealed these findings to the Department's Audit Resolution Committee (ARC), chaired by the DAG.

In June 1999, at the request of the DAG, the OIG agreed to select a sample of 40 findings for the ARC to examine in resolving the dispute. In August 1999, the Department contracted with a mediator/fact finder to resolve the disagreements between the OIG and COPS arising from this sample. Failing mediation, the mediator was asked to submit recommended findings and proposed decisions to the DAG. As formulated, the inquiry addressed whether, at the time of the audit, the grantee was in grant compliance, irrespective of whether the grantee provided such information to the OIG auditors.

Numerous meetings were held between COPS, the OIG, and the mediator. On November 1, 1999, the mediator issued a final report. In the majority of the sampled issues, either the mediator found or COPS concluded that the grantees were, as originally reported in the OIG's audit reports, not in compliance with certain grant conditions at the time of the audit. In the remaining issues, based on the totality of information available at the time of the audit-including information that was not provided by the grantees to the OIG-the mediator found that the grantees were in compliance.

On December 21, 1999, the DAG issued a Department Order in which he adopted the findings of the mediator relative to the 40 sample findings. Where the grantee was found to have been in compliance, the audit finding was closed. Where the grantee was found not to have been in compliance, COPS was ordered to obtain additional information to allow resolution of the finding or to take corrective action including the recovery of grant funds where appropriate. In addition, the DAG ordered the OIG and COPS to attempt to resolve the issues in dispute with regard to the COPS audits that were not part of the sample. COPS and the OIG held meetings to review additional information from the grantees and discuss the issues. On March 15, 2000, the DAG was advised by COPS and the OIG that, relative to the audits that were not part of the sample, no genuine disputes as to compliance remain outstanding, although several pending issues require additional information/action on the part of the grantee.

Current COPS Grant Audits

We continue to maintain extensive audit coverage of the COPS program. The Crime Act authorized $8.8 billion over six years for grants to add 100,000 police officers to the nation's streets. During this reporting period, we performed 43 audits of COPS hiring and redeployment grants. Our audits identified more than $6.8 million in questioned costs and more than $4 million in funds to better use.

The following are examples of findings reported in our audits of COPS grants during this period:

Department Financial Statement Audits

The Chief Financial Officers Act of 1990 and the Government Management Reform Act of 1994 require financial statement audits of the Department. Audit oversees and issues the reports based on the work performed by independent public accountants. During this reporting period, we issued the audit report for the Department of Justice Annual Financial Statement for FY 1999.

For the first time, the Department received an opinion on its financial statements after three years of disclaimers of opinion. The auditors issued a qualified opinion that the financial statements are presented fairly in all material respects except for the matters identified in the audit report. The qualifications in this report are because the auditors reviewing the INS accounts were unable to substantiate two significant account balances-deferred revenue and intra-governmental accounts payable.

The auditors also reported three material weaknesses and one reportable condition in the Report on Internal Controls:

In the Report on Compliance with Laws and Regulations, the auditors also identified five Department components that were not compliant with the Federal Financial Management Improvement Act of 1996 that specifically addresses the adequacy of federal financial management systems.

The following table depicts the audit results for the Department consolidated audit as well as for the 10 individual component audits for FY 1999.

| FY 1999 Audit Results | |||

|---|---|---|---|

| Reporting Entity | Auditor's Opinion on Financial Statements | Number of Reportable Conditions | |

| Material Weaknesses | Reportable Conditions | ||

| Consolidated Department of Justice | Qualified | 3 | 1 |

| Assets Forfeiture Fund and Seized Asset Deposit Fund | Unqualified | 0 | 2 |

| Bureau of Prisons | Unqualified | 0 | 2 |

| Drug Enforcement Administration | Unqualified | 4 | 6 |

| Federal Bureau of Investigation | Unqualified | 3 | 2 |

| Federal Prison Industries, Inc. | Unqualified | 0 | 0 |

| Immigration and Naturalization Service | Qualified | 4 | 4 |

| Offices, Boards, and Divisions | Unqualified | 0 | 3 |

| Office of Justice Programs | Unqualified | 1 | 5 |

| U.S. Marshals Service | Unqualified | 2 | 3 |

| Working Capital Fund | Unqualified | 0 | 1 |

The DEA's National Drug Pointer Index System

The National Drug Pointer Index System (NDPIX) is a computerized pointer system designed to provide information about ongoing drug investigations to participating federal, state, and local law enforcement agencies nationwide. NDPIX is operated and maintained by the DEA using information from participating agencies. NDPIX was developed to (1) promote information sharing; (2) facilitate drug-related investigations; (3) prevent duplicate investigations; (4) increase coordination among federal, state, and local law enforcement agencies; and (5) enhance the personal safety of law enforcement officers. The DEA estimates total costs of about $2.5 million from FY 1994 to FY 2000 for implementing and operating the system. The objectives of our audit were to (1) determine if NDPIX was adequately planned and developed, (2) evaluate the process used to deliver information to users, and (3) assess the extent to which NDPIX duplicated other law enforcement data bases.

We found that NDPIX was adequately planned and developed, does not duplicate existing systems, and can be a useful tool for improving interagency communication. However, the DEA can improve management controls over NDPIX by enhancing its measurement of NDPIX performance. In addition to counting the number of positive "hits" resulting from data entries by participating agencies as identified in its FY 1999 Performance Plan, the DEA should consider including performance measures related to NDPIX program goals, such as (1) the number of cooperative investigations resulting from positive "hits," (2) the number of arrests and convictions resulting from cooperative investigations, (3) the value of seizures resulting from such investigations, and (4) cost and time savings realized by avoiding duplicative investigations. The DEA agreed with our recommendation to develop performance measures that relate to NDPIX program goals.

The INS's Collection of Fees at Land Border Ports of Entry

INS employees at the land border POEs along the Southwest Border collect fees primarily for processing applications to replace alien registration cards, for waiver of passports and/or visas, and for nonimmigrant records of arrivals and departures. Our audit identified serious control weaknesses in the INS's fee collection program at land POEs.

In FY 1998, fee collections at all land POEs totaled approximately $17 million, with the 39 POEs along the Southwest Border accounting for more than $15 million. At five of the six Southwest Border POEs we audited, we found that cashiers could easily steal cash before it was recorded in a cash register and conceal the loss by either failing to ring up the transaction or voiding the transaction after it had been rung up. Staff responsible for handling fee monies were not held accountable for cash shortages and managers could not account for many of the cash register tapes that documented thousands of transactions. As a result, these situations left little or no audit trail and created an environment highly vulnerable to loss or theft because there was little risk of detection. Some of these conditions were first identified in a 1995 OIG audit report and have gone uncorrected despite assurances from INS management that action would be taken.

Our report contained 12 recommendations for management improvements, including updating operating procedures and distributing these procedures to employees, maintaining and reviewing cash register tapes, reconciling cash collected to applications received, conducting unannounced cash counts, and holding employees accountable for cash shortages. The INS response to our audit report did not adequately address 4 of our 12 recommendations. These four remain unresolved although the INS has agreed to implement the other eight recommendations.

The INS's Passenger Accelerated Service System

One of the INS's functions is to determine the admissibility of persons seeking entry into the United States. In an effort to facilitate the inspection process at airports, the INS developed the Passenger Accelerated Service System (INSPASS), an automated system that allows frequent business travelers who are enrolled in the program to be inspected without the assistance of an immigration inspector. At the end of FY 1998, INSPASS was deployed to six airports and facilitated approximately 146,000 admissions during the year. Through FY 1998, the INS spent more than $18 million to develop INSPASS. The objectives of our audit were to determine whether the INS had corrected problems identified in prior reviews and whether the upgraded version of INSPASS was operating effectively.

We found that the facilitation benefits provided by INSPASS in FY 1998 were insignificant because INSPASS accounted for less than 1 percent of the total admissions at the six participating airports. Additionally, we found system problems that create security risks and prevent INSPASS from reliably performing inspections. Further, the INS did not have valuable management tools, such as reliable and timely cost information, critical performance reports, and a valid cost-benefit analysis, that are necessary to make informed decisions about day-to-day operations and future expansion. We recommended that the INS correct the system problems, postpone expansion of the INSPASS eligibility criteria, and create an infrastructure that incorporates the management tools necessary to support the program. The INS's response to the audit adequately described the actions implemented and planned for 10 of the 14 recommendations. However, the INS needs to provide additional information before four recommendations can be considered resolved. This report is not currently available publicly because of the sensitivity of some items discussed in the report.

The FBI's Implementation of CALEA

Congress enacted the Communications Assistance for Law Enforcement Act (CALEA) to ensure that law enforcement agencies, when authorized by court order, had the ability to intercept electronic communications. Telecommunications carriers may be reimbursed for costs associated with equipment modifications to meet capability and capacity requirements. The Department may reimburse the carriers for the modifications from the $500 million authorized by CALEA, subject to congressional approval and availability of funds. We are required by CALEA to report to Congress by April 1, 2000, on the equipment, facilities, and services that have been modified to comply with CALEA and whether FBI payments to telecommunications carriers for equipment modifications are reasonable and cost-effective.

The FBI entered into two agreements totaling $101.8 million with a manufacturer to acquire right-to-use licenses. We found that the FBI was unable to determine the reasonableness of the manufacturer's best and final offer price for the right-to-use licenses because the manufacturer refused to provide adequate cost or pricing data. Therefore, the FBI performed alternate procurement reviews before agreeing to buy the right-to-use licenses. Absent adequate cost and pricing data from the manufacturer, we found no basis to render an opinion regarding the reasonableness of the cost incurred for the licenses.

The Government Performance and Results Act

The GPRA required the Department and other federal agencies to prepare a Strategic Plan, Annual Performance Plans, and Annual Performance Reports detailing program activities, results-oriented performance goals, and progress towards meeting goals, respectively. Our audit examined the Department's FY 2000 Summary Performance Plan to determine if it was prepared in accordance with the requirements of the GPRA and OMB Circular A-11, Preparation and Submission of Budget Estimates .

We found that the FY 2000 Summary Performance Plan generally met the requirements. However, we found that some aspects of the Plan needed improvement to fully meet the requirements. Specifically, we noted that (1) some performance goals and indicators were not measurable, (2) a discussion of how other federal agencies participate in crosscutting programs with the Department was lacking, (3) a discussion on strategies covering all performance goals was lacking, (4) resources needed to achieve results were not linked to specific performance goals, (5) some performance plans did not include performance verification and validation procedures, and (6) information on external data sources that could be used to measure performance was missing. The Department generally concurred with our specific recommendations for making future Summary Performance Plans compliant with the requirements.

Permanent Resident Aliens

The INS is required to ensure that eligible aliens in the United States who submit an Application to Register Permanent Resident or Adjust Status (I?485) have been fingerprinted and that proper background checks have been performed and reviewed. We conducted an audit of this process based on concerns noted during the INS's CUSA program, an FY 1996 initiative designed to substantially reduce the backlog of pending naturalization applications. Subsequent studies revealed that 70 percent of cases sampled lacked documentation to substantiate that fingerprint cards had been submitted to the FBI as required before naturalizations were granted. The sample consisted of about 1 million cases identified by the INS as being naturalized between August 1995 and September 1996.

Effective March 1998, all applicants for permanent resident status were required to be fingerprinted at INS Service Centers. Due to a backlog in the application processing time, we could not effectively test implementation of the new process. However, we attempted to identify opportunities for improvement in the fingerprint and application process.

We sampled 179 alien files located at three district offices and two service centers where the applications were approved during FY 1998 or FY 1999. We found that 5 of the 179 applications were incorrectly processed. We recommended that the INS implement periodic supervisory reviews of the applications to ensure the proper receipt and review of fingerprint card results prior to adjudication. The INS concurred with our recommendation.

Superfund Audit for FY 1997

The Comprehensive Environmental Response, Compensation and Liability Act of 1980 (known as Superfund) provides for liability, compensation, cleanup, and emergency response for hazardous substances released into the environment and uncontrolled and abandoned hazardous waste sites. The Department conducts and controls all litigation arising under Superfund and is reimbursed through interagency agreements with the Environmental Protection Agency (EPA). These agreements authorize reimbursement to the Environment and Natural Resources Division (ENRD) for direct and indirect litigation costs. The EPA authorized $30 million under the agreement in FY 1997, and the ENRD contracted with an accounting firm to institute and maintain a system of accounting controls for these funds.

We audited the ENRD contractor's accounting for direct and indirect costs and concluded that it presented fairly the expenses incurred in litigating Superfund cases. Specifically, our audit disclosed that (1) adequate internal controls existed to ensure the fair accumulation of costs incurred for Superfund cases and (2) costs incurred and charged to Superfund cases were properly allocated.

Trustee Audits

Audit conducts performance audits of Chapter 7 trustees under a reimbursable agreement with EOUST. Private trustees are selected and supervised by U.S. Trustees and serve on panels. The Chapter 7 trustees are appointed to collect, liquidate, and distribute personal and business cases under Chapter 7 of Title 11 of the Bankruptcy Code. As a representative of the bankruptcy estate, the Chapter 7 trustee serves as a fiduciary, protecting the interests of all estate beneficiaries, including creditors and debtors.

Audit and the EOUST recently have engaged in a cooperative effort to revise and update procedures for auditing Chapter 7 trustees. Audit formed a task group to work in cooperation with a similar group from the EOUST. Together we have modified the scope and procedures for our work to focus more intensely on areas of increasing concern to the EOUST. Significantly increased testing is now performed in the areas of asset case management and computer systems. Over the years, our cooperative effort with the EOUST has contributed to substantial improvement of trustee operations.

Single Audit Act

The Single Audit Act of 1984 requires recipients of federal funds to arrange for audits of their activities. Federal agencies that provide awards must review these audits to determine whether prompt and appropriate corrective action has been taken in response to audit findings.

During this reporting period, Audit reviewed and transmitted to the Office of Justice Programs (OJP) 73 reports encompassing 365 Department contracts, grants, and other agreements totaling more than $203 million. These audits report on financial activities, compliance with applicable laws, and the adequacy of recipients' management controls over federal expenditures.

OMB Circular A-50

OMB Circular A-50, Audit Follow-Up, requires audit reports to be resolved within six months of the audit report issuance date. The status of open audit reports is continuously monitored to track the audit resolution and closure process. As of March 31, 2000, the OIG had closed 151 audit reports and was monitoring the resolution process of 343 open audit reports.

Audits Over Six Months Old Without Management Decisions Or In Disagreement

As of March 31, 2000, the following audits had no management decision or were in disagreement:

Funds Recommended To Be Put To Better Use

| Audit Reports | Number of Audit Reports | Funds Recommended to be Put to Better Use |

|---|---|---|

| No management decision made by beginning of period | 12 | $4,136,748 |

| Issued during period | 17 | $4,109,605 |

| Needing management decision during period | 29 | $8,246,353 |

| Management decisions made during period:

--Amounts management agreed to put to better use 1 --Amounts management disagreed to put to better use |

11 3 |

$1,151,109 $345,287 |

| No management decision at end of period | 15 | $6,749,957 |

| Audit Reports | Number of Audit Reports | Total Questioned Costs (including unsupported costs) | Unsupported Costs |

|---|---|---|---|

| No management decision made by beginning of period | 46 | $12,202,161 | $5,398,727 |

| Issued during period | 58 | $8,675,524 | $1,909,968 |

| Needing management decision during period | 104 | $20,877,685 | $7,308,695 |

| Management decisions made during period: --Amount of disallowed costs1 --Amount of costs not disallowed |

472 4 |

$4,827,505 $303,017 |

$1,934,350 $184,247 |

| No management decision at end of period | 56 | $15,747,163 | $5,190,098 |

2Three audit reports were not resolved during this reporting period because management has agreed with some, but not all, of the questioned costs in the audit.

Audits Involving Recommendations For Management Improvements

| Audit Reports | Number of Audit Reports | Total Number of Management Improvements Recommended |

|---|---|---|

| No management decision made by beginning of period | 68 | 145 |

| Issued during period | 128 | 293 |

| Needing management decision during period | 196 | 438 |

| Management decisions made during period: --Number management agreed to implement1 --Number management disagreed to implement |

1162 4 |

264 15 |

| No management decision at end of period | 87 | 159 |

1Includes instances where management has taken action to resolve the issue and/or the matter is being closed because remedial action was taken.

2Includes 11 audit reports that were not resolved during this reporting period because management has agreed to implement a number of, but not all, recommended management improvements in these audits.